CGT exemption on inherited homes

Inheriting a home or a legal interest in one could be the largest windfall gain that many Australians ever experience.

There are provisions in the tax law that mean a taxpayer does not have to pay capital gains tax (CGT) when they sell a house, flat, unit or other dwelling that they have inherited. CGT is the tax paid on the profit from the sale of property or an investment.

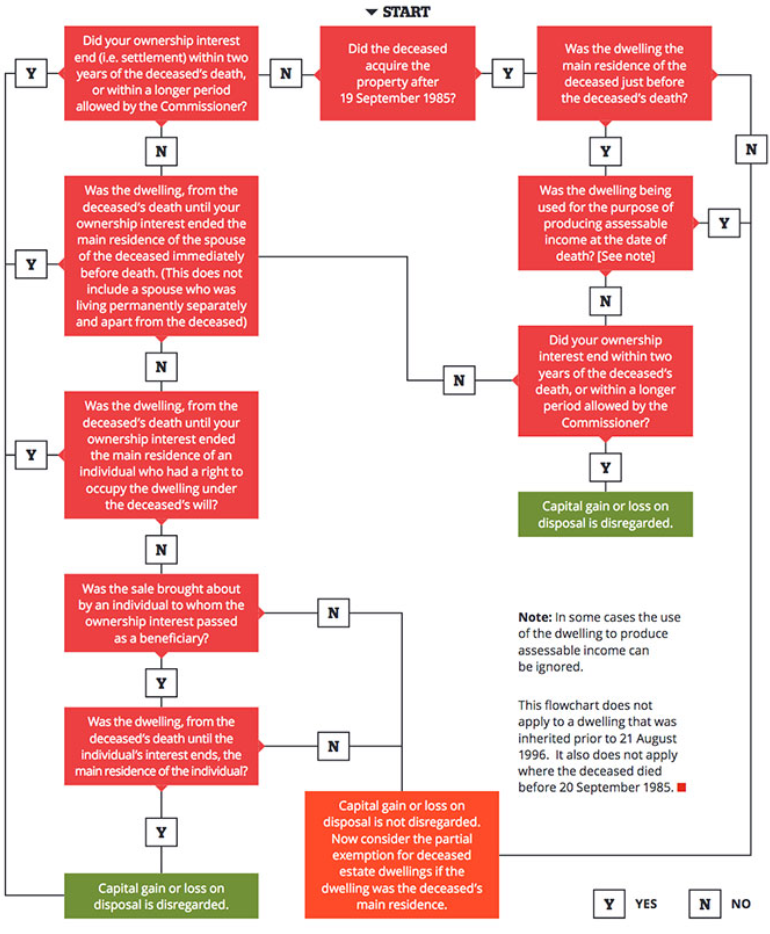

(For a quick guide, see the flowchart at the end of this post.)

Inheriting a property

From a tax law perspective, when someone dies a capital gain or loss does not apply when a property passes:

- to the deceased person’s beneficiary

- to the deceased person’s executor or other legal personal representative (LPR), or

- from the deceased’s LPR to a beneficiary.

Selling an inherited property

While generally no CGT applies when assets are distributed to beneficiaries, there may be CGT implications when the executor or beneficiary sells the inherited asset to a third party.

There are different factors that influence whether CGT will apply, including whether the asset was a pre-CGT asset or not. Assets acquired before 20 September 1985 (when CGT was introduced) are considered pre-CGT assets.

For the most part, if the beneficiary sells a dwelling within two years of the deceased’s death, then CGT does not apply. (See “The two-year rule” below).

Post-CGT assets

For dwellings acquired after 19 September 1985 to be exempt from CGT, the beneficiary must generally satisfy that the dwelling:

- was the deceased’s main residence at the time or just before their death

- was not used to produce assessable income at the time of death, and

- is sold within two years of the deceased’s death. (See “The two-year rule” below)

Note that there can be exceptions regarding whether the dwelling was a main residence before death. This includes where the owner, say, was in a nursing home before their death and the main residence was rented out. (This is known as the “absence concession”).

The two-year rule

When assessing this two-year period, where the property is sold under contract, the settlement (rather than exchange of the contract) must occur within two years of the date of death.

Note that there are some circumstances that an extension to the two-year rule may be granted.

These include (but are not limited to):

- if the ownership of a dwelling or a will is challenged

- the complexities of estate delay the completion of its administration

- a trustee or beneficiary is unable to attend to the deceased estate due to unforeseen or serious personal circumstances, and

- the settlement of a contract of sale over the dwelling is unexpectedly delayed or falls through due to circumstances outside the beneficiary or trustee’s control.

Further, if the deceased has given someone, such as a spouse or family member, a lifetime right to reside in the property, then the beneficiary may be exempt from the two-year rule. There are other circumstances where a gain can be exempt and the two-year rule has not been satisfied.

Partial exemption

Note, if the two-year deadline is not met, it doesn’t necessarily mean that the entire capital gain on the property will be subject to CGT. It may be that only part of the gain is subject to CGT, and this amount may not be significant.

Each case needs to be dealt with on an individual basis and discussed with a tax professional.