Unused super contributions

The carry-forward rules are often overlooked by eligible individuals who do not use the full amount of their concessional contributions (CCs) cap in a particular financial year.

The general concessional contributions (CCs) cap increased from $25,000 to $27,500 on 1 July 2021, and careful use of the carry-forward rules may provide additional tax and retirement planning opportunities for those eligible to use them.

Carry-forward rules recap

An individual must satisfy the following two conditions to use their unused CCs cap amounts:

- their total superannuation balance (TSB) is less than $500,000 at 30 June of the prior financial year they may be able to make the extra CCs, and

- they have unused CCs cap amounts for one or more of the previous five years in which the extra CCs are made.

The carry-forward rules allow eligible individuals to carry forward their unused CCs cap amounts from years commencing 1 July 2018 for up to five years.

The amount of the unused CCs cap is the difference between the CCs made by the individual in a financial year and the general (standard) CCs cap for that year. By carrying forward the unused cap amounts from prior years, an individual may be entitled to contribute more than the general CCs cap (currently $27,500) for the year without exceeding their CCs cap.

Practically, this means that:

- An individual cannot have unused CCs cap amounts for a financial year earlier than 2018-19. (See example 1)

- 2019-20 was the first year where an individual was able to top up CCs above the general CCs cap. (See example 2)

- An individual’s TSB is only relevant on 30 June of the year the catch‑up opportunity is actually used. This means that someone with more than $500,000 in their TSB on 30 June before one financial year could have their TSB fall below $500,000 on 30 June before a subsequent year, making them eligible to make catch up CCs in that subsequent year. Note the indexation of the general transfer balance cap (TBC) has no effect on the $500,000 TSB limit that determines whether an individual is eligible for catch up contributions, meaning this threshold has remained the same (or unchanged) after 1 July 2021. (See example 3)

- An individual’s CCs cap cannot be increased by more than the unused cap amounts from the previous five financial years and any remaining unapplied unused CCs cap is preserved and continues to be carried forward for up to five years. The amounts carried forward will expire if they remain unused after five years.

Any unused cap amounts are applied to increase an individual’s CCs cap in order from the earliest year to the most recent year. So, when an eligible individual uses some of their unused cap from prior years, the unused cap from the earliest of the five-year period is used first.

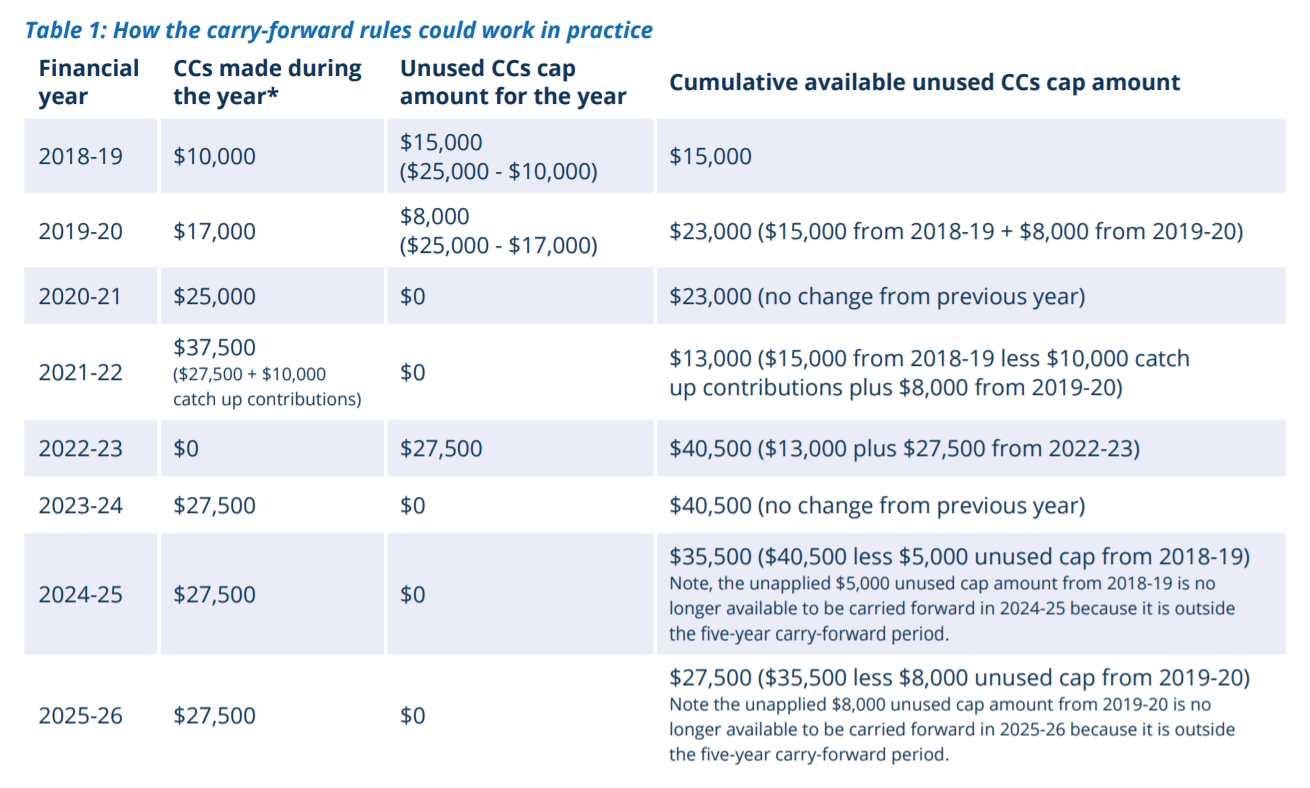

Table 1 depicts an example that illustrates how the carry-forward rules could work in practice.

From the individual perspective, there is no actual election to be made or special form to be completed when using the carryforward rules. For those eligible, the ATO will use the contributions information reported by super funds to ascertain how much unused CCs cap amount has been carried forward and how much is available to use in a year. Individuals can access their carry forward CCs using ATO online services through myGov.

However, it is important to keep in mind that due to the reporting timeframes of funds, especially SMSFs, the latest information may not be available in ATO online services. It is therefore good practice for individuals who do not use their full CCs cap each year to also keep track of all their annual super contributions as well as any catch-up CCs they make in a given year to make it easier to identify how much they can contribute in the future without exceeding their CCs cap.

Example 1

If an individual had $15,000 counted towards their CCs cap in 2017-18 and their TSB was less than $500,000 on 30 June 2018, they will be unable to carry forward the remaining $10,000 unused CCs cap amount from 2017-18 (that is, the general CCs cap of $25,000 for 2017-18 less $15,000) in the next five years because only unused amounts from 1 July 2018 onwards can be carried forward under these rules.

Example 2

If an individual had $15,000 counted towards their CCs cap in 2018-19, they would have an unused CCs amount from 2018‑19 of $10,000 that can be used/contributed in any of the next five years (ie, 2019-20, 2020-21, 2021‑22, 2022-23 and 2023-24) provided their TSB does not exceed $500,000 at 30 of June of the financial year in which they intend to use this carried forward amount.

It therefore follows that the individual in this example could use the $10,000 in say 2021-22 (in addition to their general CCs cap of $27,500) provided their TSB was less than $500,000 on 30 June 2021.

Note the leftover amount of $10,000 will be lost if it remains unused until 30 June 2024.

Example 3

An individual who has an unused CCs cap amount of $30,000 ($20,000 from 2019-20 plus $10,000 from 2020-21) and a TSB of $502,000 at 30 June 2021 would be unable to increase their general CCs cap of $27,500 to $57,500 (that is $27,500 plus $30,000) in 2021-22 by using their unused cap amounts from the previous years.

Consequently, the maximum amount they can contribute in 2021-22 without creating an excess CCs is the standard CCs cap of $27,500.

Any amounts contributed in excess of this amount will generally have to be included in the individual’s assessable income for the 2021-22 year and taxed at their marginal tax rates (with a 15% non-refundable tax offset to compensate for the tax already paid by their fund on the same excess amount).

If the individual’s TSB falls below $500,000 at 30 June 2022, the individual will be able to increase their CCs cap for the following financial year (2022-23) to $57,500 and use their $30,000 unused cap amount in that year without creating any excess CCs and therefore avoid being penalised.

As highlighted in this example, once an individual’s TSB reaches $500,000, they become limited in their contribution options.

Planning opportunities

The carry-forward provisions could play an important part in boosting the retirement savings of those with small super balances who are unable to use all of their CCs cap in a particular financial year due to broken work patterns or irregular income. Common examples of such individuals include those, mostly women, who take time out of the workforce or work part-time to care for young children or other family members, as well as those receiving irregular income (ie, farmers, small business owners, artists, etc).

The ability to use the carry‑forward rules makes it easier for those people who have a varying capacity to save from one year to the next to accumulate wealth in superannuation when they return to employment or their financial situation changes. These rules give them the opportunity to maximise their super contributions and gain the same benefits as people with regular work patterns and income who have the capacity to contribute and use their CCs cap in full each year.

The carry-forward rules may also benefit recent migrants and returned expats who have not made CCs to super in Australia. If they have funds available to make a larger CC than normally allowable under the general CCs cap, they may be able to catch up on the contributions they missed (provided they fulfil the eligibility criteria to use the carry‑forward rules)

While this is a step in the right direction for improving the flexibility for those with the opportunity to catch up, the restrictions of the five‑year carry-forward period limit the effectiveness of this measure.

Careful use of the carry-forward rules can produce tax-effective outcomes for eligible individuals who may encounter financial windfalls, such as gains on personal investments. These rules would provide the greater benefit when the individual has a known increase in income that results in changing tax brackets. By deferring making CCs to a year in which their taxable income is higher (and they are in a higher tax bracket as a result), they will be able to reduce the amount of tax they need to pay at personal level.

For example, consider an eligible individual with an average annual income who intends to sell an investment property in 2023-24 for a large capital gain that will increase their marginal tax rate to 47% (including Medicare levy). They may consider making no personal deductible contributions in 2021-22 and 2022-23 and roll their unused CCs cap amounts forward to 2023‑24 (the year the property is sold) when they can use it more effectively (provided their TSB at 30 June 2023 remains below $500,000).

In contrast, an eligible individual facing lower marginal tax rates in future years who has unused CCs cap amounts from prior years may consider using the carryforward rules this year to get a larger tax deduction and pay less tax when it will benefit them the most

Individuals wanting to use the carry‑forward rules should ensure all their CCs and available unused cap amounts are appropriately tracked and utilised to make the most of this opportunity.

If an individual is in danger of exceeding the $500,000 TSB threshold at 30 June of the prior financial year that they may be able to use the carry-forward rules, there are a number of ways to reduce their TSB

- The simplest way for those who have met a condition of release to reduce their TSB is to withdraw some of their funds from super (either as a lump sum or pension). While there is no tax payable on the additional withdrawals for those over the age of 60, any tax that will be payable by those under 60 or those withdrawing from an untaxed fund needs to be considered before adopting this strategy. Also, those in receipt of income streams that are subject to restrictions that limit the annual amount they can draw from their pensions (such as a non-commutable pension or a transition to retirement income stream) may be restricted in their ability to reduce their TSB.

- Those eligible for contributions splitting may consider splitting the CCs they made in the previous financial year to their spouse. By using this strategy to reduce their TSB below the $500,000 limit, they can make catch up contributions in the following year whilst keeping all the contributions in the superannuation environment.